Money Lessons from Mom

Written by The Inspired Investor Team

Published on May 8, 2026

minute read

Share:

In generations past, money advice often came from fathers, who were typically their family’s primary breadwinner. But times have changed: more and more mothers are the majority earner in their households,1 and it’s often moms who manage the household budget, pass on their money know-how and even inspire their kids to pursue careers in finance.

While we’re still a long way from financial gender equality in Canada – there are still pay gaps and women tend to have lower levels of financial confidence than men2 – the more that moms (and dads) talk to their kids about money, the more knowledgeable and independent the next generation will become.

As we celebrate Mother’s Day this month, we talked to four women in finance about the wisdom they learned from their moms and what some are passing down to their own children.

Jessica Moorhouse, host of the “More Money” Podcast and bestselling author of Everything but Money

My mom was the money manager in our family, and she had a big impact on me. I gleaned anything I saw her doing around figuring out our family’s budget, which was tight growing up. I learned to avoid debt as much as possible, because that can be very expensive, and not to buy things you can’t afford with cash.

One of my mom’s key lessons was really knowing where your money is and taking control of it – that’s something I learned early on, and I’m lucky that I did. I had friends in university who would just spend money, and I thought that was so interesting, because I was told that there’s a finite amount of money, so you need to really be strategic with it. I’ve never had consumer debt in my life, probably because of what I saw from my mom. Just living below your means was really, really important.

The most important thing is that she’s always been very consistent. Now my dad’s retired and my mom is retiring very soon, so I’m able to already see the benefits of sticking to what she’s told me. They have a paid-off house, they have all these fruits of their labour, and so that’s really nice to see – that the proof is in the pudding.

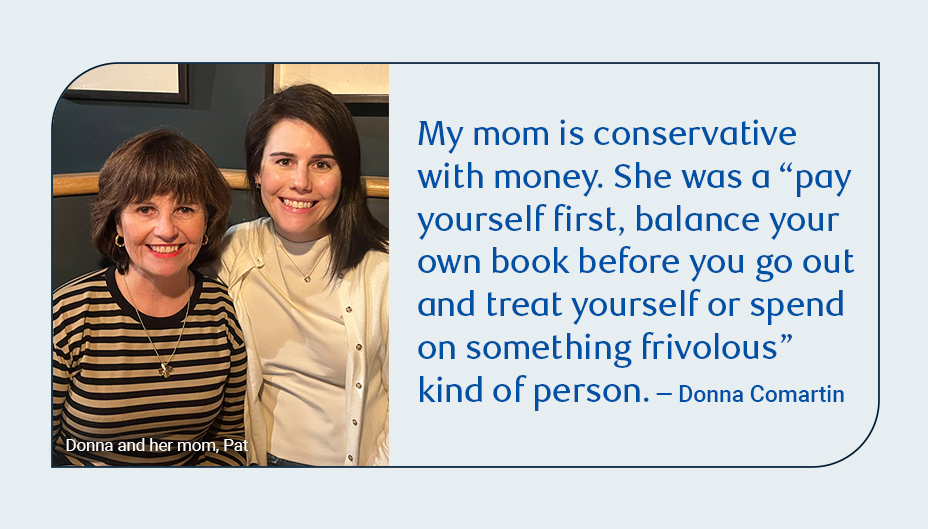

Donna Comartin, Portfolio Manager, North American Equities at RBC Global Asset Management

My mom was always very pragmatic. Her famous line for me and my sister when we’d fall or have a bad day was that “it won’t kill you.” It always sounded harsh, but she meant “let’s look at the big picture here, and don’t sweat the small stuff.” That’s an important lesson for investing. You need to filter out the noise, resist the urge to panic trade during volatility, be emotionally disciplined and focus on the fundamentals. Really, it’s looking at the long term. Women have a reputation of being hysterical, and she’s really not. She has framed a lot of how I think about stressful situations.

My mom is conservative with money. She was a “pay yourself first, balance your own book before you go out and treat yourself or spend on something frivolous” kind of person. When we were growing up, she would never put groceries on a credit card, because she thought, “I need to be able to pay for these groceries.” Credit card debt was all the rage in the ’90s, but she didn’t use her credit card, even when she didn’t have a lot of money, and she always talked about that.

I have a child of my own, and if I have advice for her and the next generation, it’s that you have time. Invest early and often. A lot of my friends and family feel intimidated by investing, and it should not be that way. The best investors aren’t always the smartest – they’re the most consistent. Regular saving and disciplined, diversified investing in quality companies is often likely to serve you well.

Angelica Murison, Senior Portfolio Manager, North American Equities, RBC Global Asset Management

My parents divorced when I was four years old. Unfortunately, money was always a source of conflict, so while I was growing up, my mother taught me to never rely on anyone but myself, which was a monumental life lesson. As a single immigrant mother working to support three kids, her life was not easy; however, seeing my mother struggle with finances, along with raising my brothers and I, resulted in me being hyper-focused on independence, and it instilled in me a strong work ethic.

Despite my husband being an investment banker, I run our household finances. I have spreadsheets that model out our incomes and savings until retirement, and I tinker with different assumptions. It’s rare for a woman to control the household finances, but my mom taught me that women need be on top of everything because, at the end of the day, your life is your responsibility.

One of the main reasons I chose this career is because of how focused I became on financial literacy and financial stability, which unfortunately a lot of young women aren’t well versed in, as schools don’t teach much of this. My sons are only seven and four, but I’m extremely frank with them and tell them constantly that everything in the world costs money – going out to dinner, the house we live in, playing hockey – so they have to study and work hard, and have successful careers. I want to impart to them how important savings and financial literacy are, even if they’re too young to fully grasp the concept. Although my childhood was a bit tough, I am so thankful for the lessons it taught me, and so grateful for my mother, who shaped me into the woman I am today.

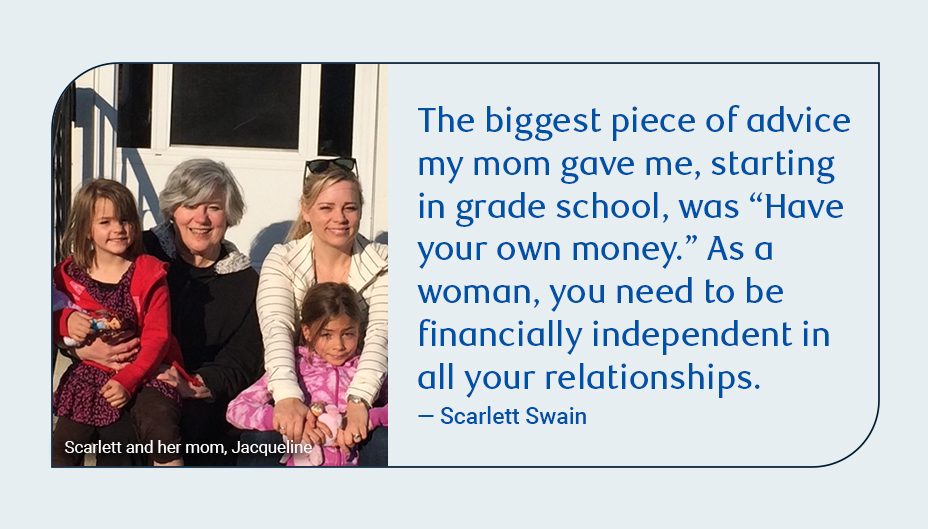

Scarlett Swain, Vice-President, Transformation, RBC Direct Investing

The biggest piece of advice my mom gave me, starting in grade school, was “Have your own money.” As a woman, you need to be financially independent in all your relationships. Make your own money and look after it, because it’s the source of your power and decision-making.

My mom also taught me the importance of living within your means and saving for the future. We’re kind of a “Wealthy Barber” family, taking the approach of “pay yourself first.” When I got my first part-time job, my mom negotiated with me that I would give her half of each paycheque and she would put it into a separate account for me to save for school and all the things I would want to do. At the time, that felt really steep. But when I got into university, my parents gave me a lump sum of money, part of which was my own savings. And I’m actually doing that with my two kids as well. We have a spreadsheet where I show them the interest they’re earning. And now, as they’re moving into university and summer jobs are harder to find, they see the importance of that safety net. There really is a circle of life, when it comes to teaching people about money.

As I’ve grown into working in the financial industry, the more interesting question has become “How do you grow your money? How do you make sure you’ve got sustainable income?” But it’s all rooted in making sure you have your own source of income and control over your funds, and that you’re paying close attention to what your money’s doing and how it’s working for you.

Our research at RBC Direct Investing found something interesting: the first direct investing account that most women open is an RESP. I wasn’t surprised, because the things moms do for their kids is always above and beyond the things they do for themselves. And it’s actually true for me – my first investing accounts were my kids’ RESPs, and there was a long gap before I applied what I’d learned to myself and maximized my RRSP and TFSA. It’s so important for women not to have dependence on anyone. You’re the caretaker of your future, and you create your own wealth, so be mindful, be thoughtful, be forward-looking.

- The Vanier Institute of the Family, “Families Count 2024”, November 2024

- Journal of Financial Literacy and Wellbeing, “Increasing financial confidence in Canadian women”, January 2026

RBC Direct Investing Inc. and Royal Bank of Canada are separate corporate entities which are affiliated. RBC Direct Investing Inc. is a wholly owned subsidiary of Royal Bank of Canada and is a Member of the Canadian Investment Regulatory Organization and the Canadian Investor Protection Fund. Royal Bank of Canada and certain of its issuers are related to RBC Direct Investing Inc. RBC Direct Investing Inc. does not provide investment advice or recommendations regarding the purchase or sale of any securities. Investors are responsible for their own investment decisions. RBC Direct Investing is a business name used by RBC Direct Investing Inc. ® / ™ Trademark(s) of Royal Bank of Canada. RBC and Royal Bank are registered trademarks of Royal Bank of Canada. Used under licence.

© Royal Bank of Canada 2026.

Any information, opinions or views provided in this document, including hyperlinks to the RBC Direct Investing Inc. website or the websites of its affiliates or third parties, are for your general information only, and are not intended to provide legal, investment, financial, accounting, tax or other professional advice. While information presented is believed to be factual and current, its accuracy is not guaranteed and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the author(s) as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by RBC Direct Investing Inc. or its affiliates. You should consult with your advisor before taking any action based upon the information contained in this document.

Furthermore, the products, services and securities referred to in this publication are only available in Canada and other jurisdictions where they may be legally offered for sale. Information available on the RBC Direct Investing website is intended for access by residents of Canada only, and should not be accessed from any jurisdiction outside Canada.

Explore More

ETF Trends from the RBC Capital Markets Trading Floor – June 2026

Here’s what we saw on the trading floor in June 2026

minute read

3 Things We’re Watching This Week: Canada-U.S. Summit, GLP-1s, Canadian Energy

What the Inspired Investor team is watching this week

minute read

Pause, Verify, Decide: How to Spot & Stop Financial Scams

What to know about the most common scams circulating today as artificial intelligence makes them more convincing

minute read

Inspired Investor brings you personal stories, timely information and expert insights to empower your investment decisions. Visit About Us to find out more.